Are the Magnificent 7 Still Magnificent?

Extraordinary performance is a challenge to prudent diversification

The Mag 7 continue to outpace the market. In after-hours trading last night, Nvidia jumped another 6% in 75 minutes. Does this mean you should pile on? For most investors the answer is no.

Long-term investors don’t seek the highest return regardless of risk. Picking stocks and chasing trends is rarely successful over full market cycles. They seek optimal risk-adjusted return with the goal of maximizing return while minimizing risk.

Recent stock market returns have been remarkable – up 31% since early April. But in times of exuberance, people forget about risk. A long-running study by DALBAR shows that mutual fund investors do worse than the mutual funds themselves. Driven by emotion, individual investors tend to buy high and sell low. Now is the time to ease up on our collective obsession with returns and focus on controlling risk.

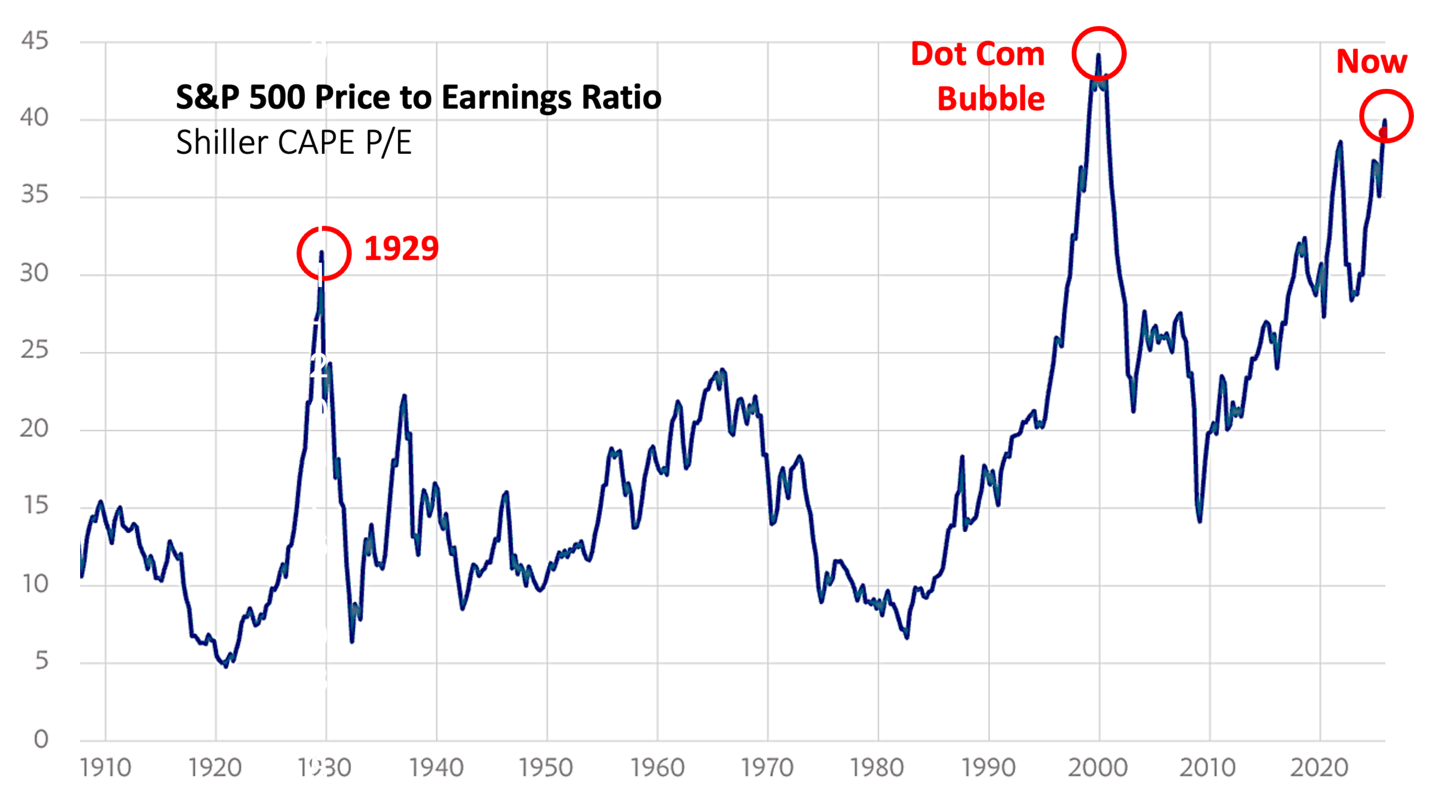

Today, there are two caution signs: valuation and concentration. The stock market is trading at elevated valuations. That doesn’t mean it will tumble or crash any time soon. No one can know that and certainly not me. However, as measured by historical price-to-earnings ratios, valuations are the highest they’ve been since the dot com bubble in 2000.

25 years ago, I lived through the Internet frenzy when I was CEO of PayPal. Like everyone else in Silicon Valley, I repeated the mantra that “this time is different”. The Internet was going to change the world. It did, but it took a long time. When markets are high, there is less headroom to rise and farther to fall.

A disproportionate share of the rise comes from the Magnificent 7 largest tech stocks – Nvidia, Microsoft, Apple, Google, Amazon, Meta and Tesla. Ten years ago, they represented 12% of the value of the entire S&P 500. Today they weigh in at an astounding 35%. Because the S&P 500 represents half of the total global equity value, these seven companies are almost one fifth of the value of all public companies in the world.

The Mag 7 accounted for 56% of total return of the S&P 500 in 2022, 63% in 2023, and 55% in 2024 and about 40% so far this year. Notably, the growth in value is supported by growth in earnings. Except for Nvidia which has the magic formula of high growth and high profitability and Tesla which has ... robots?, the P/E ratios of the Mag 7 are not out of line with the market.

Nevertheless, this extreme concentration is a challenge to your portfolio. The time-tested way to reduce concentration risk is through diversification, but it’s hard to diversify away from one fifth of the global market. Because these large tech companies tend to move together, they pose an unprecedented and undiversified risk within the S&P 500, which is the most common investment for those seeking broad diversification.

What can you do? First, don’t fall into the trap of thinking you’re smarter than everyone else and start chasing hot stocks. Second, if the tech sector is overweighted in your portfolio, rebalance your equity holdings. Third, consider underweighting the Mag 7. Fourth, if the run up in stocks has misaligned your stock/bond/cash ratio, rebalance your asset allocation. What did Warren Buffet do? He put over $300 billion into U.S. Treasuries.

In the market, emotion is your enemy. Nobel Prize winner Richard Thaler calls it the “hot hands fallacy”. When a player sinks five baskets in a row, fans are convinced he’ll sink the sixth. The statistics show there is no such thing. Good times won’t last forever, so don’t be fooled.

What’s the definition of a lucky investor? A rising market and a short memory.

The information presented is for general informational and educational purposes only and does not constitute personalized investment advice or a recommendation to buy or sell any specific securities or investment strategies. All investing involves risk, including the potential loss of principal, and past performance is not indicative of future results. The views expressed are those of the author as of the date indicated and may change without notice. Any forward-looking statements are not guarantees of future performance.